Since, I never mind being a guinea pig (no racial slurs please) I figured I could dole out some credit advice on two fronts. (I decided to check my credit today as part of the Federal Act that allow for

Free Annual Credit Reports (NY just came online).

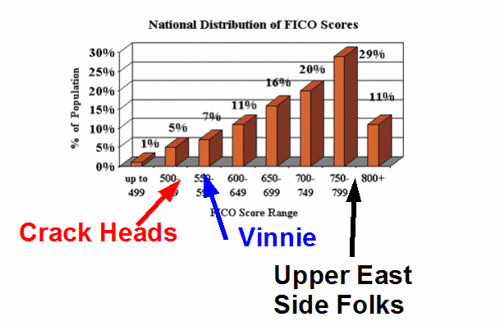

So two pieces of advice I can dole out, #1, cell phone disputes go onto your credit report, #2 Maxing out a ridicoulous amount of debt is bad. Note, there are 3 credit reporting agencies in the U.S.: Experian, TransUnion, and Equifax.

#1I'm currently disputing my Verizon bill because they raped me with overage charges and I switched providers. (Sprint PCS has a

Fair & Flexible plan that I always tout, you never have to worry about going 'over' your minutes.)

I had the incorrect hope that my Verizon dispute wouldn't make it into my credit report from what I've seen from previous credit reports. It has not shown up on the Experian report but has showed up on the other two reports. As I am still contesting the amount they say I owe and I have send them payment of what I feel I owe, I still think I can have it knocked off my credit reports, (at least I hope).

So my advice hear, is that if you cut your cell phone contract early, it WILL go on your credit report. However, for me, I don't mind as I have a few reasons to disupte the charge and I belive I can get it off my credit report during the next few months.

#2Now this is the important infomation. Last year I had the idea to take out a whole bunch of 0% credit cards and drop them into an

ING Bank account (currently 3.3% interest). So while that's all working out and I make almost $100 month for doing nothing, it has a severe impact on your credit report.

A fact I knew going into it. I wasn't worried as I belive once I pay the cards back at the end of this year, my credit score will begin increasing again. So while this is not worth while to the majority of people, I didn't mind giving it a try.

Here are more detailed explanations of the two items above.

For Item #1, Verizon dispute:

-Evidence of being seriously late or having derogatory indicators/remarks on your credit obligations is being reported on your credit file

You have evidence of seriously delinquent behavior (60 days past due or greater). Approximately 27% of U.S. population have evidence of serious delinquency information being reported on their credit file.

The score evaluates when your credit bureau report shows one or more serious delinquencies (missed payments) on your credit accounts. Studies reveal that consumers with previous late payments are much more likely to pay late in the future.

There is no "quick fix" to improve the score if the serious delinquency indicated on your credit bureau report is valid. However, as these items age and fall off the credit bureau report (most late payments stay on your report for no more than seven years), their impact on the score will gradually decrease

-The time since your most recent past due payment or derogatory indicator is too recent or unknown

There is evidence of a late payment on your file as recent as 2 months ago. Roughly 45% of consumers have some evidence of delinquency in their credit history. Among these consumers, their most recent late payment was, on average, 20 months ago. Click here to review your Negative Items.

Analysis of consumer credit histories shows that consumers with previous late payments are much more likely to pay late in the future. The FICO score evaluates not only the presence of previous late payments, but also how recently the missed payments occurred. In general, the more recently a payment was missed, the greater the risk, and the lower the score. (Most late payments stay on your report for no more than seven years. Keep in mind that closing an account on which you had previously missed a payment does not make the late payment disappear from your credit bureau report.) In rare cases, evidence of a past missed payment on a credit account is present on the credit report, but the date of the late payment cannot be determined exactly. An "undateable" credit account delinquency on a credit report still represents greater risk than never having missed a payment at all, and so it will still affect the score.

There is no "quick fix" to raise your score if the late payment on your credit bureau report is valid. In order to improve your credit rating over time, it's important to pay all bills when they're due. The longer you do so, the better the score. If you have late payments, get caught up on them and do your best to stay current. As time passes the importance of these previous late payments will gradually lessen and the score will increase - as long as you make your payments on time on all of your credit obligations, and use your available credit responsibly.

For Item #2, taking out a lot of Credit Cards in a short period of time and running them to the max :)

-The proportion of balances to credit limits on your revolving accounts is too high

The proportion of balances to credit limits (high credit) on your revolving accounts is 71%. The average proportion of balances to credit limits on revolving accounts carried by U.S. consumers is around 40%. Click here to review your Accounts Summary.

Analysis of consumer credit behavior repeatedly finds that owing a substantial balance on revolving accounts (Visa, MasterCard, Discover, American Express, department store cards, etc.) relative to the amount of revolving credit available to you represents increased risk. In fact, the level of revolving debt is one of the most important factors in the FICO score. The score evaluates your total balances in relation to your total available credit on revolving accounts, as well as on individual revolving accounts. For a given amount of revolving credit available, a greater amount owed indicates a greater risk, and lowers the score. (For credit cards, the total outstanding balance on your last statement is generally the amount that will show in your credit bureau report. Bear in mind that even if you pay off your credit cards in full each and every month, your credit bureau report may show the last billing statement balance on those accounts.)

The more you owe on revolving credit accounts - relative to the amount of credit available to you - the more your score may be affected. So doing your best to pay your revolving account balances is a smart way to help increase your score. On the other hand, shifting balances among revolving accounts, opening up new revolving accounts, and closing down other revolving accounts will not improve your score, and could possibly decrease your score.

-The length of time your accounts have been established is relatively short

Your most established credit obligation is 104 months old and your newest credit account was opened 10 months ago. The majority of U.S. consumers have a relatively long credit history - with the average age of their most established credit account being 14 to 15 years. In addition, the average time since the most recent account opening is 20 months ago. Click here to review your Accounts Summary.

This factor is based on the age of the accounts on your credit bureau report (the age of the oldest account, the average age of accounts, or both). Research shows that consumers with longer credit histories have better repayment risk than those with shorter credit histories. Also, consumers who frequently open new accounts have greater repayment risk than those who don't.

It is a good idea to only apply for credit when you really need it. Meanwhile, maintain low-to-moderate balances and be sure to make your payments on time. Your score should improve as your credit history ages.

-You have too many accounts that were recently opened

On average, U.S. consumers recently opened about 1 new credit obligation.

Analysis repeatedly finds that opening several credit accounts in a short period of time represents increased risk for future repayment--especially for consumers who do not have a long credit history. As you demonstrate that you can manage these new credit obligations over time, your score will reflect that positive behavior.

One immediate step you can take is to avoid opening more accounts at this time. Beyond that, the most effective way to improve your score is by following the tried-and-true rules of personal finance: manage all your accounts responsibly - including new ones - and do your best to make all your payments on time.

-You have a relatively high number of accounts with balances

On average, U.S consumers carry balances on approximately 4 of their credit accounts at a given time.

Analysis repeatedly finds that carrying balances on too many credit accounts at once is a predictor of future repayment risk. (For credit cards, note that even if you pay off your balance in full every month, your credit bureau report may still show a balance on those cards. The total balance on your last statement is generally the amount that will show in your credit bureau report.)

In order to improve your FICO score, pay down the balances on your credit obligations. For revolving accounts, once they are paid down keep your balances low.

Hopefully this information can be of benefit to people searching for these answers. I wish I knew how much it affected my credit report. Because Experian doesn't list my Verizon dispute, I can estimate that costing around 120 points (out of 850). I think it's so large of a hit because it's recent (~2-3 months). If it was a few years old, I don't think it would hurt as much.

As for the max'd credit cards (with a VERY LARGE amount of debt) I can only guess, I would guess around a 100-200 point hit. Again, I think this will improve over the next year. As I knew I wouldn't be applying for any loans while I had these 0% CC's max'd out, I was okay for what I would walk into.

I can wait it out.